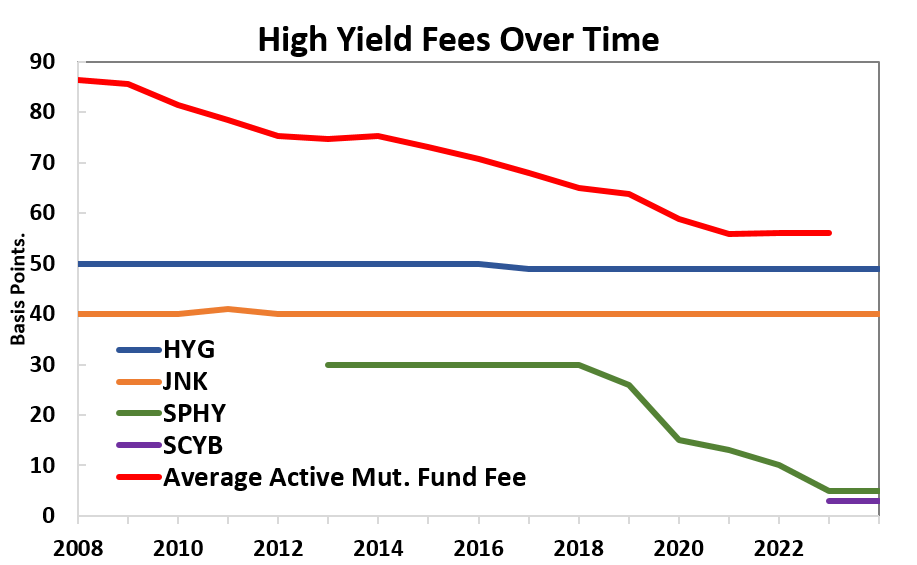

The declining costs of investing is a boon for investors. Even individual investors can own efficient cap-weighted portfolios of stocks and bonds for less than 5 basis points (bps). Beyond major market exposures, competition between index providers is driving down investing costs in another market, high yield bonds. Ten years ago, the average actively managed high yield fund charged 75 bps and the cheapest index option charged 30 bps. Today, these fees are 56 bps for active and 3 bps for index. Lower fees make high yield a more compelling investment option than it had been previously.

Total investment performance is viewed in terms of active management (alpha) plus market returns (beta). Fees also have both active and beta components. The net active fee is the difference between the active manager’s fee and the cost to index. For example, the average high yield mutual fund fee was 71 bps in 2016, which was 41 bps more than the 2016 fee of the State Street HY ETF: SPHY. That 41 bps represents the net cost of active management. Fast forward to today, the spread between the average active mutual fund and the cheapest index product is 53 bps. Lower index fees make net active management fees more expensive if active managers do not adjust fees down as indexing becomes cheaper. As the chart show, active fees for high yield have been falling with index fees.

Creating efficient index exposure in high yield has been a challenge for ETF providers. Dealing with bonds migrating in and out of the index, focusing holdings on the most liquid portion of the junk bond market, and managing customer cash flows has been difficult for high yield ETFs. The two largest high yield ETFs (HYG and JNK) are in the bottom decile of the institutional high yield performance peer group over the last 15 years. Outperforming high yield benchmarks has also been difficult for active managers, but most have performed better than the ETFs.

For the high yield market tactically, Concord’s outlook is cautious as yields are attractive, but spreads are tight in front of what may become a more unfavorable economic backdrop. Structurally, lower management fees allow investors to keep more of their high yield investment’s yield, making the asset class more compelling.