The concentration of equity returns across a small group of companies creates challenges for asset allocators and opportunities for wealth creation for investors. The AI-driven rally in Nvidia highlights the changing nature of equity growth and the importance of participating in it. A phenomenon called the “network effect“ partially explains some of the exuberance around these stocks.

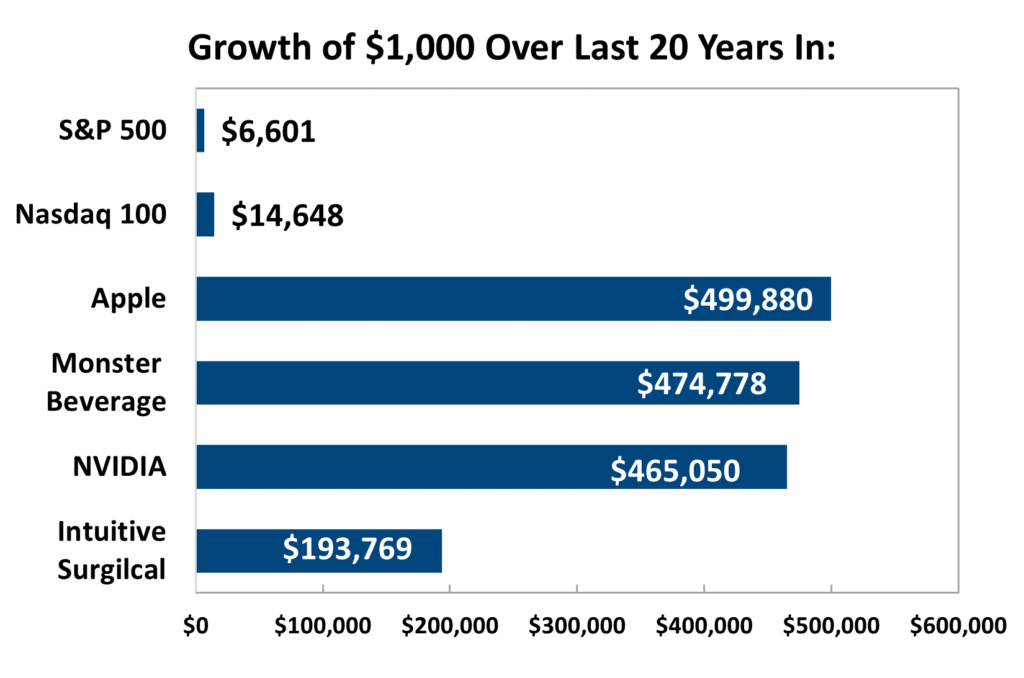

Apple, the best performing S&P 500 stock over the last 20 years, is a good example of a company leveraging network effects. As the number of Apple iPhone users increases, iPhone features such as FaceTime and AirDrop become more useful. This attracts more iPhone users, which further improves the iPhone network, creating a positive feedback loop. In a comparable manner, as more customers buy iPhones, software developers are more incentivized to create apps for the IOS platform, which motivates more people by buy iPhones.

These positive feedback loops can create exponential growth, drive stock prices higher, and make it difficult for other firms to compete. Microsoft’s software, Google’s search & YouTube, Netflix, Nvidia’s architecture, and Amazon Marketplace are platforms and stocks that have benefitted from positive network feedback loops.

The growing influence of network effects on companies is challenging some of the tried-and-true rules of investing. For example, a portfolio of 95% S&P 500 / 5% Apple stock at the start of 2004, left untouched, would have an allocation of 68% S&P/ 32% Apple five years later. Conventional financial advice would recommend reducing the Apple position, as the portfolio is insufficiently diversified and has too much concentration in one stock. However, Apple kept outperforming for another 15 years.

The Apple example is an extreme case, and this is not a recommendation to chase the Magnificent 7 stocks. Owning the S&P 500 provides sufficient exposure to these stocks; Magnificent 7 stocks have a 29% weight in the S&P 500. Considering the power of network effects, along with the observation that stock indices give higher weights to more successful companies, it is not surprising that active large cap managers have struggled to compete with the S&P 500.