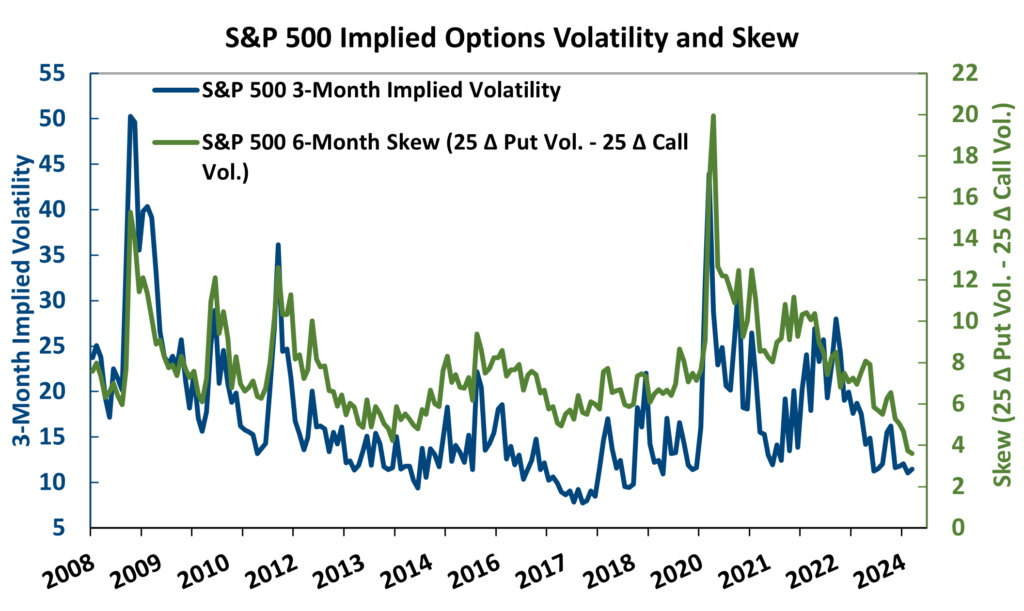

Investment markets have been very calm this year, and the cost of buying insurance on the equity market with options has rarely been cheaper. On the chart below, the blue line plots the historic implied volatility of S&P 500 options. Higher levels of implied volatility equate to options being more expensive, and the current environment of low implied volatilities means that purchasing options is less expensive than it had been in most prior periods.

One step deeper, the green line shows the put call skew. Skew in options is the implied volatility difference between out of the money (OTM) puts and calls. The implied volatility premium of puts over calls is at its lowest level since 2007. The low levels of volatility and skew make the cost to hedge equity downside risk historically inexpensive. [Concord monitors volatility and skew to assess market sentiment. This is not a recommendation to hedge portfolios with options.]

There are theories to explain or interpret the current cheapness in hedging downside equity market risk. One attributes the cheapness to investors allocating $64 Billion into ETFs designed to sell options, thereby driving options prices lower. It is also possible that fear of missing out, ”FOMO,” on the AI boom has increased demand for call options. Late economist Hyman Minsky would have seen the current stability as long-term destabilizing, a signal that the market was becoming too complacent on risk. Others argue a technology and service-based economy, with more government safeguards and backstops on banks, is less prone to shocks. There are elements of truth in all these theories. Thus far in 2024, the equity market has been remarkable for being unremarkable.