There is an interesting debate about a contract between Chicago Bears rookie defensive lineman Gervon Dexter and an entity called Big League Advance Fund II (BLA). While a student at the University of Florida, Dexter signed a contract with BLA. In the contract, BLA agreed to pay Dexter $436,485 upfront, and Dexter agreed to pay BLA 15 percent of his pre-tax future professional football earnings for the next 25 years. Dexter signed a 4-year, $6.7 million dollar contract with the Bears; therefore, BLA stands to receive about $1 million from Dexter. Dexter is suing BLA to void the contract. Many people see this deal as predatory and wrong (which it may very well be), but the analysis of the contract is not as straightforward as it may appear.

BLA’s motivation in the contract is easy to understand. BLA is a wealth maximizing, risk taking, investor willing to risk $436,000 because the expected value of 15 percent of Dexter’s future NFL earnings was greater than that amount.

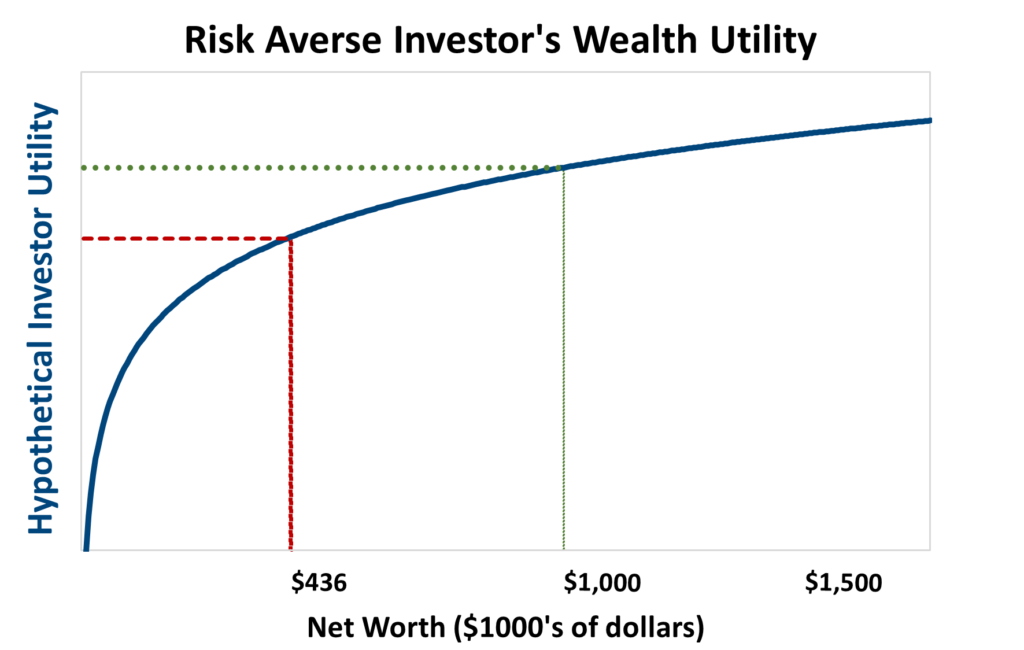

Without knowing Mr. Dexter’s risk tolerance or then financial status, his signing of the contract implies risk aversion and a need for a risk-free payment. In the chart, we drew a representation of a wealth utility function for a risk averse investor. The vertical axis is the amount of utility, i.e., happiness, a person derives from a given level of wealth on the horizontal axis. For someone with a low starting level of wealth, a $436,000 upfront payment provides a larger increase in utility than increasing their wealth from $436,000 to $1 million. Gervon Dexter’s deal with BLA did not maximize the expected value of his wealth, but reduced risk (mainly from injury) and likely provided a significant increase in utility.

With cash rates at 5% nominal and the financial world less predictable after Covid and associated inflation, this is an opportune time to reevaluate the capacity to assume risk. Some institutional investors may find it wise to create a safe bucket of assets, earning 5%, and then invest the balance to maximize returns and expected value, like Mr. Dexter. Others may be able to invest more opportunistically and maximize expected value as BLA does. Neither is wrong. Wealth utility is an important but illusive and hard to quantify concept that varies from investor to investor.